RMS Response to Forecast Evaluation

December 7th, 2007Posted by: Roger Pielke, Jr.

Robert Muir-Woods of RMS has graciously provided for posting a response to the thoughts on forecast verification that I posted earlier this week. Here are his comments:

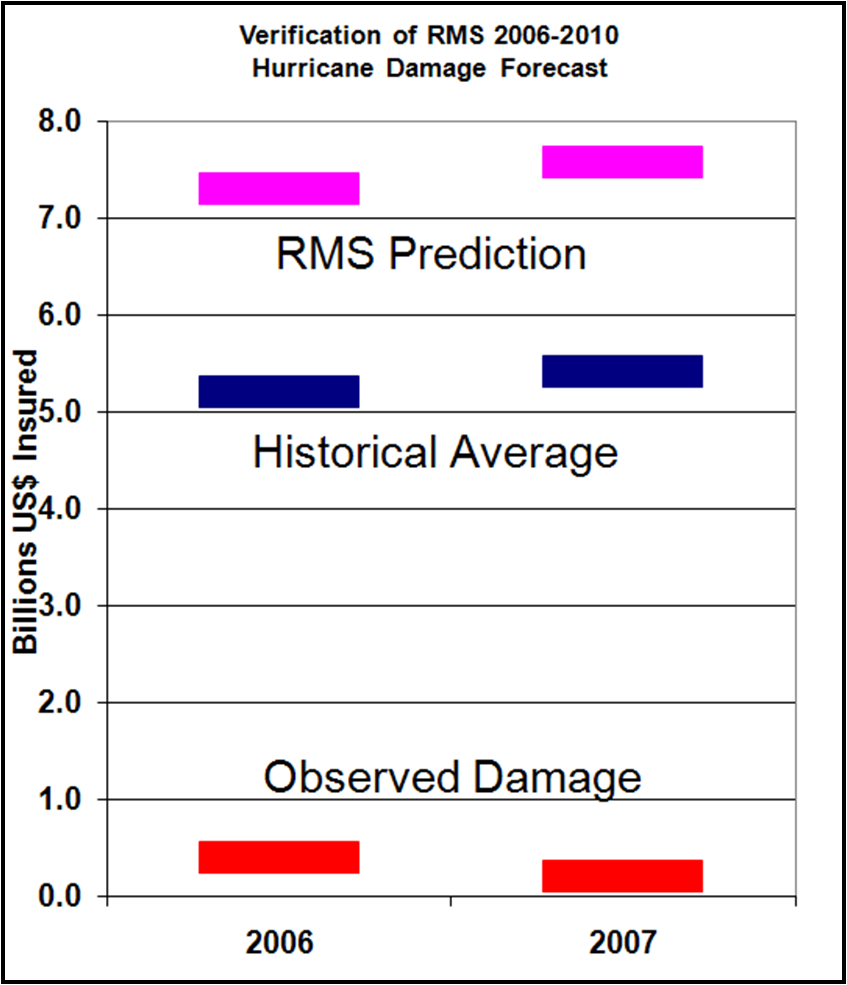

Scientifically it is of course not possible to draw any conclusion from the occurrence of two years without hurricane losses in the US, in particular following two years with the highest level of hurricane losses ever recorded and the highest ever number of severe hurricanes making landfall in a two year period. Even including 2006 and 2007, average annualized losses for the past five years are significantly higher than the long term historical average (and maybe you should also show this five year average on your plot?)

The basis for catastrophe loss modeling is that one can separate out the question of activity rate from the question as to the magnitude of losses that will be generated by the occurrence of hurricane events. In generating average annualized losses we need to explore the full ‘virtual spectrum’ of all the possible events that can occur. The question about current activity rates is a difficult one, which is why we continue to involve some of the leading hurricane climatologists, and a very wide range of forecasting methodologies, in our annual hurricane activity rate update procedure. In October 2007 an independent expert panel concluded that activity rates are forecasted to remain elevated for the next five years. While this perspective was announced and articulated by RMS, we did not originate it. Each year we undertake this exercise, we ensure that the forecasting models used to estimate activity over the next five years also reflect any additional learning from the forecasting of previous years, including the low activity experienced in 2006 and 2007. We don’t ‘declare success’ that the activity rate estimate that has emerged from this procedure over the past three years (using different forecast models and different climatologists) has scarcely changed, but the consistency in the three 5 year projections is interesting nonetheless.

You may also be surprised to learn that our five-year forward-looking perspective on hurricane risk does not inevitably produce higher losses than all other models, which use the extrapolation of the simple long-term average to estimate future activity. This is as shown in a comparison published in a report prepared by the Florida Commission on Hurricane Loss Projection Methodology for the Florida House of Representatives (see the Table 1 on page 25 of the report, which can be downloaded from here: http://www.sbafla.com/methodology/announcements.asp?FormMode=Call&LinkType=Section&Section=0)

Robert Muir-Wood

RMS